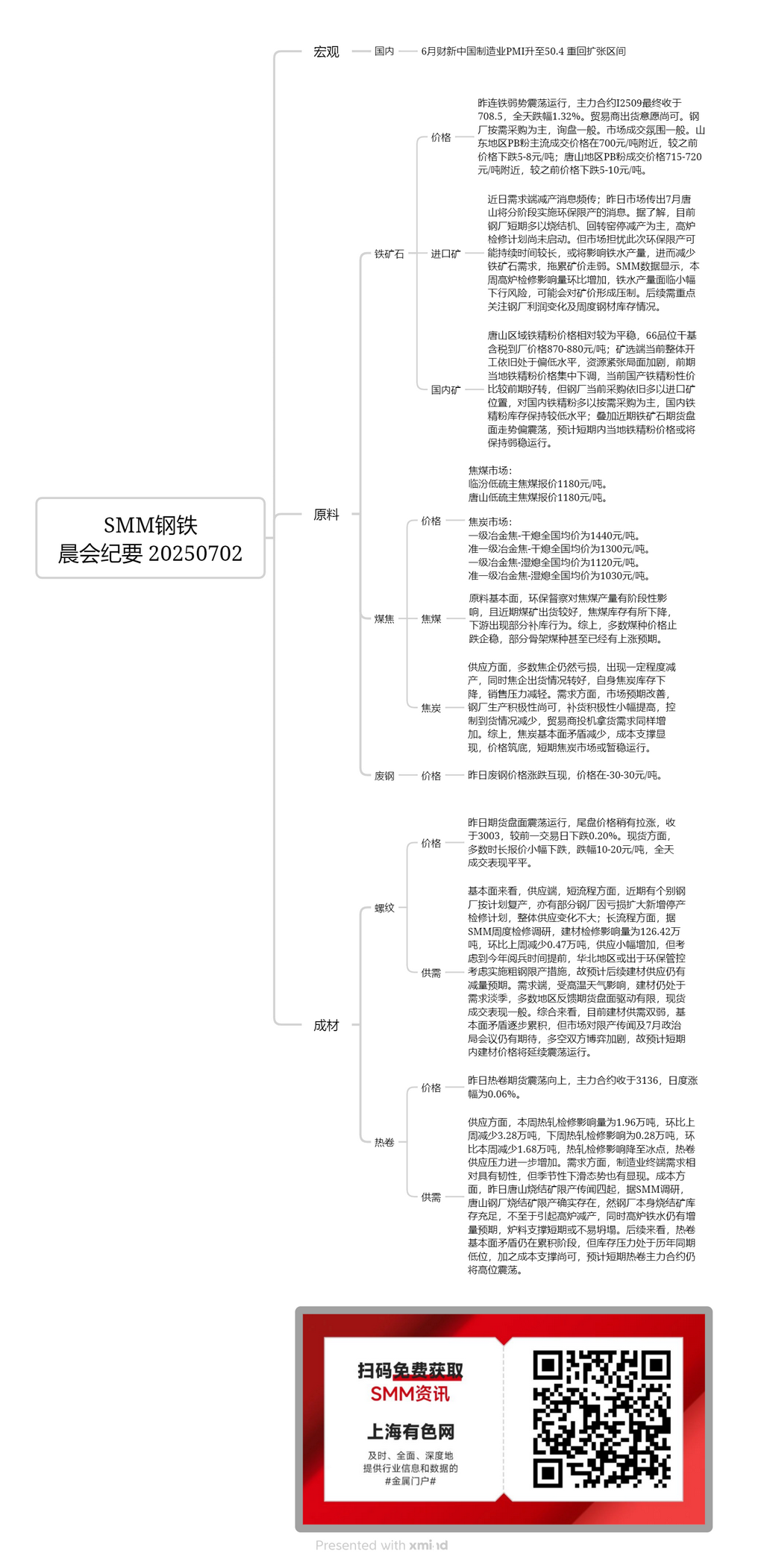

Domestic ore:

Prices of 66-grade iron ore concentrates in Tangshan remained relatively stable, with delivery-to-factory prices (tax included) at 870-880 yuan/mt. Mines and beneficiation plants continued to operate at low capacity, exacerbating tight supply. Following previous price cuts, domestic iron ore concentrates now offer better cost-performance compared to earlier periods. However, steel mills still prioritize imported ore, purchasing domestic concentrates mainly as needed, keeping inventories low. Coupled with recent volatile futures market trends, local iron ore concentrate prices are expected to remain in the doldrums in the short term.

Imported ore:

The most-traded i2509 contract closed at 708.5 yesterday, down 1.32% for the day, as futures market remained in the doldrums. Traders showed moderate willingness to sell, while steel mills mainly purchased as needed with limited inquiries. Market transactions were subdued. In Shandong, mainstream transaction prices for PB fines hovered around 700 yuan/mt, down 5-8 yuan/mt from previous levels; Tangshan PB fines traded at 715-720 yuan/mt, down 5-10 yuan/mt. Recent market rumors suggested Tangshan would implement phased environmental protection-driven production restrictions in July. Currently, steel mills have temporarily suspended or reduced sintering machine and rotary kiln operations, though blast furnace maintenance plans remain unexecuted. Concerns persist that prolonged restrictions may reduce pig iron production, dampening iron ore demand and weighing on ore prices. SMM data showed blast furnace maintenance impact increased WoW, posing slight downside risks to pig iron production, which may pressure ore prices. Future focus should center on steel mill profits and weekly steel inventory changes.

Coking coal:

Low-sulphur coking coal in Linfen was quoted at 1,180 yuan/mt, while Tangshan prices stood at 1,180 yuan/mt. Environmental protection checks temporarily affected coking coal production. Recent strong mine shipments reduced inventories, prompting some downstream restocking. Consequently, most coal prices stopped falling and stabilized, with some key grades even showing upward potential.

Coke:

Nationwide average prices were: first-grade metallurgical coke (dry quenching) at 1,440 yuan/mt, quasi-first-grade (dry quenching) at 1,300 yuan/mt, first-grade (wet quenching) at 1,120 yuan/mt, and quasi-first-grade (wet quenching) at 1,030 yuan/mt. Supply side, most coking plants remained loss-making, implementing production cuts. Improved shipments reduced coke inventories, easing sales pressure. Demand side, market sentiment improved as steel mills maintained moderate production enthusiasm, slightly increasing restocking activity while reducing delivery controls. Traders also showed growing speculative purchasing demand. In summary, the fundamental contradictions in the coke market have decreased, cost support has emerged, prices have bottomed out, and the coke market may stabilize temporarily in the short term.

Rebar:

Yesterday, the futures market fluctuated, with prices slightly rallying towards the end of the session, closing at 3003, down 0.20% from the previous trading day. In the spot market, most quotes dropped slightly, with declines ranging from 10-20 yuan/mt, and overall trading performance was mediocre. From a fundamental perspective, in terms of supply, for the short-process production, a few steel mills have resumed production as planned, while some others have added new shutdown and maintenance plans due to expanding losses, resulting in relatively small overall supply changes. For the long-process production, according to the SMM weekly maintenance survey, the impact from maintenance on building materials was 1.2642 million mt, a decrease of 4,700 mt WoW, indicating a slight increase in supply. However, considering the earlier military parade this year, North China may implement crude steel production restrictions due to environmental protection-related controls, so it is expected that there will still be a reduction in building material supply in the future. On the demand side, affected by high temperatures, building materials remain in the off-season for demand, with most regions reporting limited driving force from the futures market and mediocre spot trading performance. Overall, currently, both supply and demand for building materials are weak, and fundamental contradictions are gradually accumulating. However, the market still has expectations for rumors of production restrictions and the July Political Bureau meeting, intensifying the battle between bulls and bears. Therefore, it is expected that building material prices will continue to fluctuate in the short term.

HRC:

Yesterday, HRC futures rose amid fluctuations, with the most-traded contract closing at 3136, up 0.06% on a daily basis. In terms of supply, the impact from maintenance on hot-rolled production this week was 19,600 mt, a decrease of 32,800 mt WoW. Next week, the impact from maintenance on hot-rolled production is expected to be 2,800 mt, a decrease of 16,800 mt from this week. The impact from maintenance on hot-rolled production has reached its lowest point, further increasing the supply pressure for HRC. On the demand side, terminal demand in the manufacturing sector remains relatively resilient, but seasonal decline trends have also emerged. In terms of costs, rumors of sinter production restrictions in Tangshan spread yesterday. According to the SMM survey, sinter production restrictions in Tangshan steel mills do exist. However, the steel mills themselves have sufficient sinter inventories, which will not lead to blast furnace production cuts. Meanwhile, there is still an expectation for an increase in blast furnace pig iron, so furnace charge support may not collapse easily in the short term. Looking ahead, the fundamental contradictions in the HRC market are still in the accumulation stage, but inventory pressure is at a low level compared to the same period in previous years. Coupled with moderate cost support, it is expected that the most-traded HRC futures contract will continue to fluctuate at highs in the short term.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)